Data tokens on this page

Beneficial Owner Form

What You Need to Know

Beneficial Owner Form

What You Need to Know

The CDD Rule: What It Means For You

The U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) has put a new Customer Due Diligence (CDD) Rule in place that requires financial institutions to collect additional information to verify the identity of certain types of owners, and top level officials, of legal entities opening or making changes to accounts.

The CDD Rule strengthens regulations already in place to help the government fight financial crime like terrorist financing, money laundering, tax evasion, corruption, and fraud. Requiring that financial institutions verify key individuals who own or control a legal entity helps law enforcement prevent and prosecute these crimes.

What is Considered a Legal Entity Under the CDD Rule?

A legal entity client is a corporation, limited liability company, or other entity that is created by the filing of a public document with a Secretary of State or similar office, a general partnership, and any similar entity formed under the laws of a foreign jurisdiction.

CERTAIN ENTITIES ARE EXCLUDED ENTIRELY AND ARE NOT SUBJECT TO THE CDD RULE:

- Individuals opening accounts on their own behalf

- Federally regulated financial institutions or state regulated banks

- Federal or state government departments, agencies, or political subdivisions

- Entities established by federal or state governments on behalf of the government

- Entities other than banks publicly traded on NYSE, NASDAQ, or ASE

- Domestic entities with at least 51 percent owned by an entity traded on NYSE, NASDAQ, or ASE

- Issuer of securities under section 12 of Securities Exchange Act

- Investment companies and investment advisers

- Exchange or clearing agencies

- Other entities registered with the SEC

- Entities registered under Commodity Exchange Act, registered with CFTC

- Public accounting firms registered under Section 102 of Sarbanes-Oxley Act

- Bank holding companies

- Insurance companies regulated by a state

- Sole proprietorships or unincorporated associations

- Estates and personal trusts

CERTAIN CUSTOMER TYPES ONLY REQUIRE INFORMATION AND SIGN-OFF OF THE CONTROLLING PARTY.

Beneficial Ownership is not required for these entities:

- Charities, nonprofits, public benefit corporations

- Small social community organization, like Girl Scout troops and sports leagues

- Non-excluded pooled investment vehicles

What is The Difference Between Ownership and Control Components?

OWNERSHIP: All of those that exercise control through direct or indirect ownership of the legal entity are identified under the ownership component. These are individuals or entities with an ownership interest in the legal entity client (i.e. shares or stock in a corporation, membership interests in a limited liability company etc.) or serve as a trustee for a trust with an ownership interest in the legal entity client. All of those individuals who exercise control through their roles within the management structure of a legal entity are identified under the control component.

CONTROL: Control over Entity individuals have significant responsibility to control, manage, or direct the non-individual client (i.e. CEO, CFO, COO, managing member, general partner, etc.). One individual could satisfy both the ownership and control components if the individual meets both definitions.

Whose Information Do We Need?

The CDD Rule requires that we identify, verify, and keep records of beneficial owners and controlling party information for our legal entity customers at the time of account opening or at the point of a significant change to an account. That means each individual who owns 25 percent or more of the equity interest and an individual who has significant managerial control over the entity: that may be a single individual. Each entity may have between one and five individuals, one person under the control category and up to four owners.

What Information Needs to be Provided for the Beneficial Owner and Controlling Party?

✔ Name, date of birth, address

✔ Social security number for U.S. residents; passport number or other similar information for foreigners

✔ A valid US government issued ID (i.e. driver’s license, state ID, alien registration card, U.S. passport, or a matricula card). One of these pieces of identification needs to be entered into the system as primary ID.

✔ A completed and verified certification form at account opening

Who is Responsible for Calculating Legal Ownership Percentages?

The customer is responsible for determining the percentages of ownership for both direct and indirect owners.

EXAMPLE 1

If DOE INC. is owned by John Doe and Mary Doe (50 percent each) then their information would be collected since they each own 25 percent or above.

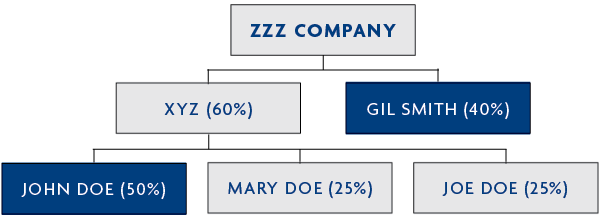

EXAMPLE 2

If ZZZ Company is owned, 60 percent by XYZ partnership and 40 percent by Gil Smith, then the customer would need to determine who the owners of XYZ partnership are. If John Doe owns 50 percent of XYZ partnership, then his indirect ownership percentage equals 30 percent (multiplying 60 percent by 50 percent). Using similar calculation Mary and Joe indirectly own 15 percent each of ZZZ (multiplying 60 percent by 25 percent). Gil’s and John’s information would be collected since they own 40 percent and 30 percent of ZZZ respectively.

Although the customer is responsible for these calculations, the bank should be prepared to explain how to calculate the indirect ownership percentages if the customer asks.

Who Signs the Certification of Beneficial Owners Form?

The individual providing the information used to open the account is the person who is required to sign the Certification of Beneficial Owners form. This person may or may not be an owner or associated person on the non-individual account.